Introduction

Definition of Blockchain

Blockchain is a revolutionary technology that has gained widespread attention in recent years. It is a decentralized and distributed digital ledger that records transactions across multiple computers or nodes. The key feature of blockchain is its ability to ensure transparency, security, and immutability of data. In simple terms, it is a chain of blocks, where each block contains a list of transactions. These blocks are linked together using cryptographic hashes, forming a chronological and unalterable chain. Blockchain technology has the potential to disrupt various industries, including finance, supply chain, healthcare, and more, by providing a trusted and efficient way of recording and verifying transactions.

Brief History of Blockchain

Blockchain technology has a rich and fascinating history that dates back to the early 2000s. It all started with the concept of a decentralized digital currency, which was first introduced by an anonymous person or group of people using the pseudonym Satoshi Nakamoto. In 2008, Nakamoto published a whitepaper titled ‘Bitcoin: A Peer-to-Peer Electronic Cash System’, which outlined the fundamental principles of blockchain technology. This revolutionary technology gained significant attention and became the foundation for the development of cryptocurrencies, including Bitcoin. Since then, blockchain has evolved and expanded its applications beyond digital currencies, with industries such as finance, supply chain, healthcare, and more exploring its potential. Today, blockchain is recognized as a transformative technology that offers transparency, security, and efficiency in various sectors.

Importance of Blockchain Technology

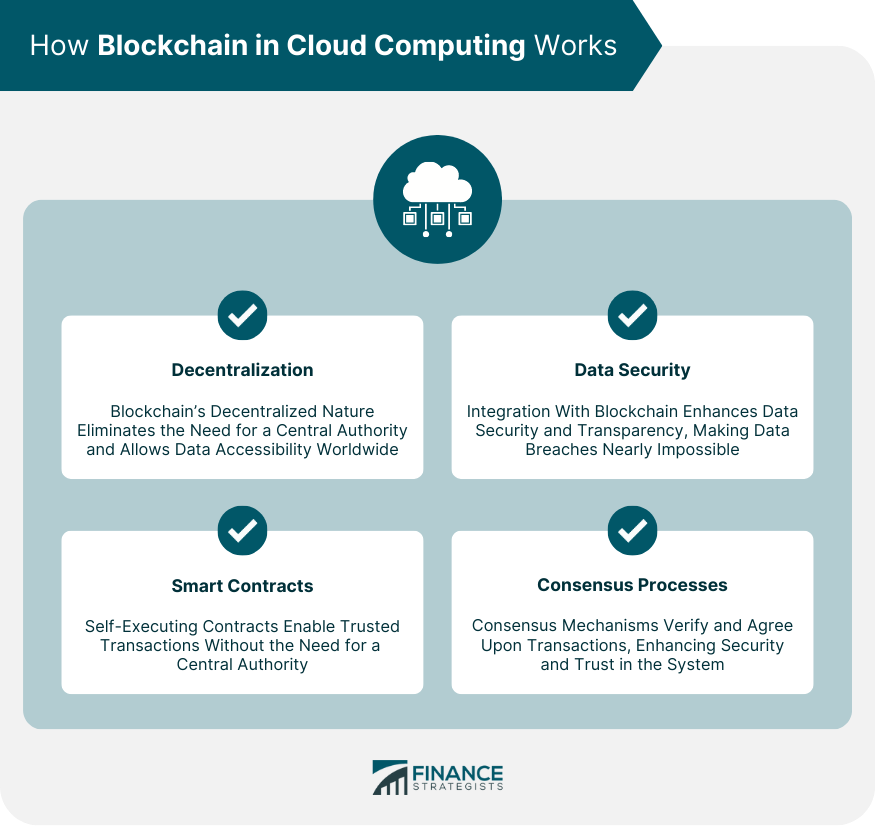

Blockchain technology is of great importance in today’s digital world. It has revolutionized various industries by providing secure and transparent transactions. With its decentralized nature, blockchain eliminates the need for intermediaries, making transactions faster and more efficient. Moreover, the immutability of blockchain ensures that data cannot be tampered with, enhancing trust and reliability. The importance of blockchain technology extends beyond finance and has potential applications in healthcare, supply chain management, and voting systems, among others. As more businesses and organizations recognize the benefits of blockchain, its adoption is expected to increase exponentially in the coming years.

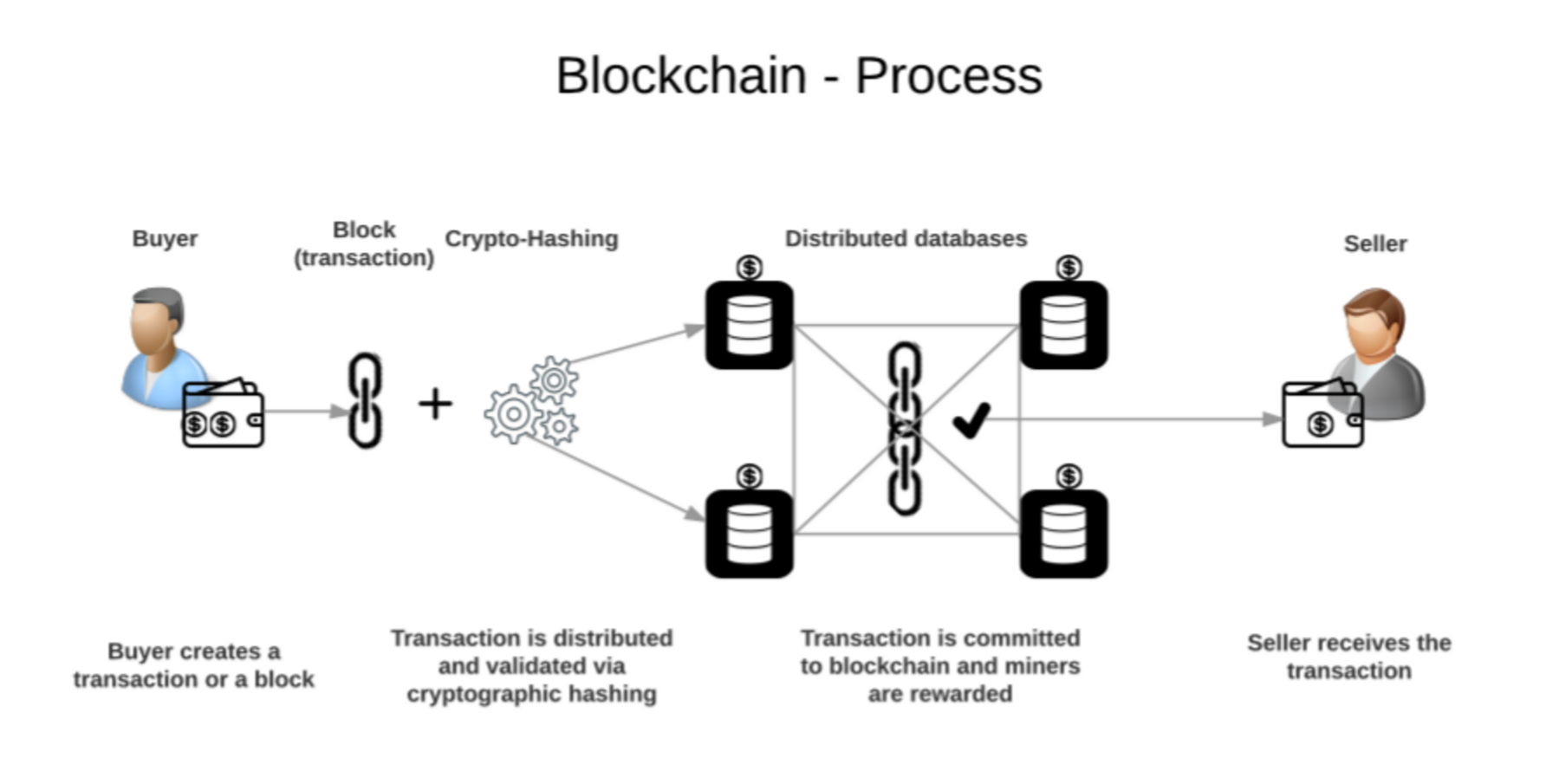

How Blockchain Works

Decentralized Network

A decentralized network is a fundamental aspect of blockchain technology. Unlike traditional centralized systems, where a single authority controls and verifies transactions, a decentralized network allows multiple participants, known as nodes, to maintain and validate the blockchain. This distributed nature of the network ensures transparency, immutability, and security. Each node in the network holds a copy of the entire blockchain, and any changes or updates to the blockchain require consensus from a majority of the nodes. This decentralized approach eliminates the need for intermediaries, reduces the risk of fraud, and enhances the resilience of the system against attacks or failures. Overall, a decentralized network is the cornerstone of blockchain technology, enabling trustless and peer-to-peer transactions on a global scale.

Consensus Mechanism

Blockchain technology relies on a consensus mechanism to ensure the accuracy and security of transactions. The consensus mechanism is a set of rules and protocols that all participants in the blockchain network must follow to reach an agreement on the validity of transactions. One commonly used consensus mechanism is Proof of Work (PoW), where participants compete to solve complex mathematical puzzles to validate transactions and add them to the blockchain. Another popular consensus mechanism is Proof of Stake (PoS), where participants are chosen to validate transactions based on the number of coins they hold. Each consensus mechanism has its own advantages and disadvantages, and the choice of mechanism depends on the specific goals and requirements of the blockchain network.

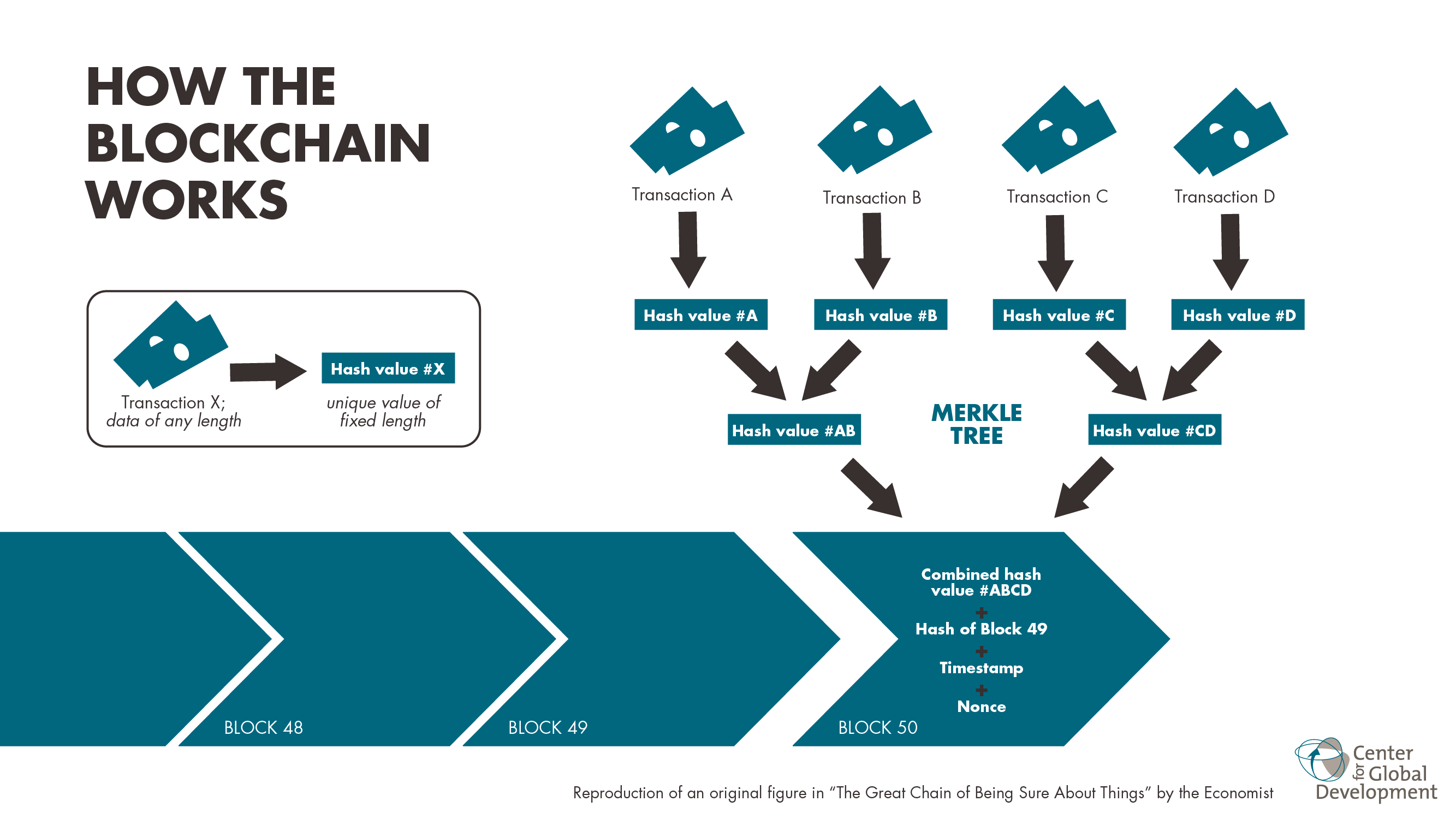

Cryptographic Hash Function

A cryptographic hash function is a fundamental component of blockchain technology. It is a mathematical algorithm that takes an input (or message) and produces a fixed-size string of characters, which is typically a hash value or hash code. This hash value is unique to the input data, meaning that even a small change in the input will result in a completely different hash value. This property makes cryptographic hash functions ideal for ensuring data integrity and security in blockchain networks. By using hash functions, blockchain systems can verify the integrity of data stored in blocks and detect any tampering attempts. Additionally, cryptographic hash functions play a crucial role in linking blocks together in a chain-like structure, enabling the immutability and transparency of blockchain technology.

Key Components of Blockchain

Blocks

Blocks are an essential component of blockchain technology. They are the building blocks that make up the entire blockchain network. Each block contains a set of transactions that have been verified and added to the blockchain. Blocks are linked together in a chronological order, creating a chain of blocks. This ensures the immutability and security of the data stored on the blockchain. Additionally, blocks also contain a unique identifier called a hash, which is generated using a cryptographic algorithm. This hash serves as a digital fingerprint for the block, making it easy to verify its integrity. Overall, blocks play a crucial role in maintaining the integrity, transparency, and decentralization of the blockchain technology.

Transactions

Transactions are a fundamental concept in blockchain technology. They represent the transfer of value from one party to another on the blockchain network. When a transaction occurs, it is recorded on the blockchain as a permanent and immutable record. This ensures transparency and security, as all participants on the network can verify and validate the transaction. Transactions in blockchain technology are typically peer-to-peer, meaning they do not require intermediaries such as banks or payment processors. This eliminates the need for trust in third parties and allows for faster and more efficient transactions. Overall, transactions play a crucial role in the functioning of blockchain technology, enabling secure and decentralized value transfer.

Public and Private Keys

Public and private keys are fundamental components of blockchain technology. These keys play a crucial role in ensuring the security and integrity of transactions on the blockchain. Public keys are used to encrypt data and verify digital signatures, while private keys are used to decrypt data and create digital signatures. The combination of these keys enables secure and tamper-proof communication between participants in a blockchain network. By using public and private keys, blockchain technology provides a decentralized and transparent way of conducting transactions, where trust is established through cryptographic algorithms rather than relying on intermediaries or central authorities.

Types of Blockchain

Public Blockchain

A public blockchain is a decentralized network that allows anyone to participate and validate transactions. It operates on a consensus mechanism, where multiple nodes in the network agree on the validity of transactions. Public blockchains are transparent, as all transactions and data are visible to anyone on the network. This transparency ensures trust and security, as it prevents any single entity from controlling or manipulating the blockchain. Public blockchains are often used for cryptocurrencies, such as Bitcoin and Ethereum, but they can also be utilized for various other applications, such as supply chain management and voting systems.

Private Blockchain

Private blockchains are a type of blockchain that restricts access to its participants, making it suitable for organizations that require a higher level of privacy and control over their data. Unlike public blockchains, where anyone can participate and validate transactions, private blockchains are typically permissioned, meaning that only approved entities can join the network. This allows organizations to maintain strict control over who can access and interact with the blockchain, ensuring that sensitive information remains secure. Private blockchains are often used in industries such as finance, healthcare, and supply chain management, where data privacy and confidentiality are of utmost importance.

Consortium Blockchain

A consortium blockchain is a type of blockchain that is governed by a group of organizations rather than a single entity. In a consortium blockchain, multiple organizations come together to form a network and collectively validate and maintain the blockchain. This type of blockchain is often used in industries where multiple stakeholders need to collaborate and share information securely, such as supply chain management or financial services. The governance structure of a consortium blockchain allows for greater transparency and accountability among the participating organizations, as decisions regarding the blockchain’s rules and operations are made collectively. Additionally, consortium blockchains can offer increased scalability and privacy compared to public blockchains, as access to the network and participation in consensus mechanisms are restricted to the consortium members.

Applications of Blockchain

Cryptocurrencies

Cryptocurrencies have emerged as one of the most significant applications of blockchain technology. These digital currencies use cryptographic techniques to secure transactions and control the creation of new units. Bitcoin, the first and most well-known cryptocurrency, paved the way for the development of numerous other cryptocurrencies such as Ethereum, Ripple, and Litecoin. Cryptocurrencies offer decentralized and transparent systems for exchanging value, eliminating the need for intermediaries like banks. They provide users with greater financial autonomy and privacy, as transactions are recorded on a public ledger called the blockchain. With the increasing popularity of cryptocurrencies, their impact on various industries and the global economy continues to grow.

Supply Chain Management

Supply chain management is a crucial aspect of any business, and with the advent of blockchain technology, it has become even more efficient and transparent. Blockchain allows for the secure and decentralized tracking of products throughout the entire supply chain, from raw materials to the end consumer. This technology provides a tamper-proof record of every transaction and movement, ensuring that the supply chain is free from fraud, counterfeiting, and other malpractices. By leveraging blockchain, businesses can improve inventory management, reduce costs, and enhance customer trust. In addition, blockchain enables real-time visibility into the supply chain, allowing for faster problem identification and resolution. With its potential to revolutionize supply chain management, blockchain is set to reshape the way businesses operate in the future.

Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into lines of code. These contracts automatically execute when the specified conditions are met, eliminating the need for intermediaries or third parties. By using blockchain technology, smart contracts provide transparency, security, and efficiency in various industries such as finance, supply chain management, and healthcare. They enable parties to trust the outcome of the contract without relying on a central authority, making transactions faster, cheaper, and more reliable. With the potential to revolutionize traditional contract management, smart contracts are a key component of blockchain technology.

Challenges and Future of Blockchain

Scalability

Scalability is a crucial aspect of blockchain technology. As the popularity of blockchain continues to grow, it is important to address the issue of scalability. Scalability refers to the ability of a blockchain network to handle a large number of transactions efficiently. With the increasing adoption of blockchain in various industries, such as finance, supply chain, and healthcare, the demand for a scalable blockchain solution is more pressing than ever. Blockchain developers and researchers are constantly exploring innovative techniques and solutions to improve the scalability of blockchain networks. These efforts include the implementation of sharding, layer-two protocols, and consensus algorithms that can handle high transaction volumes without compromising security or decentralization. Achieving scalability in blockchain technology is essential for its widespread adoption and realization of its full potential.

Regulatory Concerns

Regulatory concerns play a crucial role in the adoption and implementation of blockchain technology. As this innovative technology disrupts traditional industries and challenges existing regulatory frameworks, governments around the world are grappling with how to effectively regulate and monitor blockchain-based systems. One of the main concerns is the potential for money laundering and illicit activities facilitated by the anonymity and decentralized nature of blockchain networks. Additionally, issues related to data privacy, consumer protection, and intellectual property rights need to be addressed to ensure a safe and fair environment for all stakeholders involved. Despite these challenges, regulators are recognizing the potential benefits of blockchain technology and are actively working towards developing comprehensive regulatory frameworks that balance innovation and protection.

Interoperability

Interoperability is a crucial aspect of blockchain technology. It refers to the ability of different blockchain networks to communicate and interact with each other seamlessly. In a decentralized ecosystem, where multiple blockchain platforms exist, interoperability ensures that these platforms can share data, assets, and functionalities without any hindrance. This allows for the seamless transfer of value and information between different blockchain networks, enhancing the overall efficiency and effectiveness of the technology. Interoperability also promotes collaboration and innovation, as developers can leverage the strengths of various blockchain platforms to create more advanced and versatile applications. As the blockchain industry continues to grow, achieving interoperability will be essential for realizing the full potential of this transformative technology.