Introduction

Definition of blockchain

Blockchain is a decentralized and distributed ledger technology that allows multiple parties to record and verify transactions in a secure and transparent manner. It is essentially a chain of blocks, where each block contains a list of transactions that have been validated and added to the chain. The key feature of blockchain is its immutability, meaning that once a transaction is recorded, it cannot be altered or tampered with. This makes blockchain an ideal solution for industries that require trust, security, and transparency, such as finance, supply chain management, and healthcare. By implementing blockchain in business, organizations can benefit from increased efficiency, reduced costs, improved security, and enhanced trust among stakeholders.

Overview of blockchain technology

Blockchain technology is a revolutionary concept that has the potential to transform various industries. It is a decentralized and transparent digital ledger that securely records and verifies transactions. The technology provides numerous benefits, including enhanced security, increased efficiency, and improved traceability. By eliminating the need for intermediaries and enabling peer-to-peer transactions, blockchain can streamline business processes and reduce costs. Additionally, the immutability of blockchain ensures data integrity, making it highly resistant to fraud and tampering. With its ability to create trust and enable secure transactions, blockchain technology offers immense potential for businesses to innovate and gain a competitive edge in today’s digital economy.

Importance of blockchain in business

Blockchain technology has become increasingly important in the business world due to its numerous benefits. One of the key advantages of implementing blockchain in business is the enhanced security it provides. With its decentralized and immutable nature, blockchain ensures that data cannot be tampered with or altered, making it highly secure and resistant to hacking. Additionally, blockchain offers transparency by allowing all participants in a network to have access to the same information, promoting trust and accountability. Moreover, blockchain streamlines processes by eliminating the need for intermediaries and reducing transaction costs. By implementing blockchain, businesses can improve efficiency, reduce fraud, and enhance overall operations. As a result, the importance of blockchain in business cannot be overstated, as it has the potential to revolutionize industries and drive innovation.

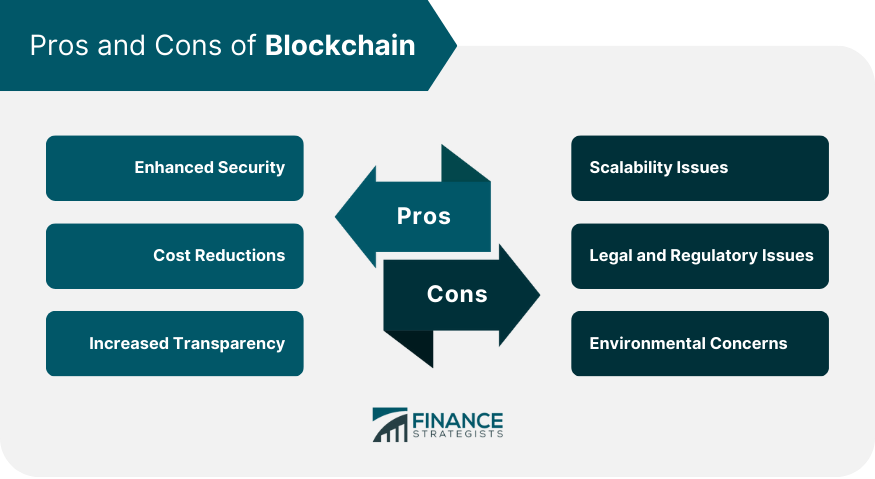

Enhanced Security

Immutable and transparent transactions

Blockchain technology enables immutable and transparent transactions, revolutionizing the way businesses operate. By leveraging the decentralized nature of blockchain, transactions are recorded on a public ledger that is accessible to all participants, ensuring transparency and eliminating the need for intermediaries. The immutability of the blockchain ensures that once a transaction is recorded, it cannot be altered or tampered with, providing a high level of security and trust. This transparency and immutability not only streamline business processes but also enhance accountability and reduce the risk of fraud. Implementing blockchain in business offers numerous benefits, including increased efficiency, cost savings, and improved customer trust.

Decentralized network

A decentralized network is one of the key features of blockchain technology. Unlike traditional centralized systems, where a single authority controls the flow of information and transactions, a decentralized network allows for peer-to-peer interactions, eliminating the need for intermediaries. This not only enhances security and transparency but also promotes trust and reliability. By removing the reliance on a central authority, blockchain technology empowers individuals and businesses to have more control over their data and transactions, leading to increased efficiency and cost savings. Additionally, the decentralized nature of blockchain makes it resistant to censorship and tampering, further ensuring the integrity of the network. Overall, implementing a decentralized network through blockchain technology offers numerous benefits for businesses, including increased security, transparency, efficiency, and trustworthiness.

Protection against fraud and data tampering

Blockchain technology provides businesses with a robust solution for protecting against fraud and data tampering. By its very nature, blockchain is designed to be transparent, immutable, and decentralized. This means that once data is recorded on the blockchain, it cannot be altered or tampered with without the consensus of the network participants. This level of security makes blockchain particularly valuable in industries where trust and data integrity are critical, such as finance, supply chain management, and healthcare. With blockchain, businesses can have confidence that their data is secure and protected from unauthorized access or manipulation, providing a strong defense against fraud and ensuring the integrity of their operations.

Efficiency and Cost Savings

Streamlined processes

Blockchain technology has revolutionized the way businesses operate by streamlining processes. With its decentralized and transparent nature, blockchain eliminates the need for intermediaries, reducing costs and increasing efficiency. By providing a single source of truth, blockchain ensures data integrity and enhances trust among stakeholders. Additionally, smart contracts enable automated and secure transactions, eliminating the need for manual verification and reducing the risk of fraud. Overall, implementing blockchain in business leads to streamlined processes, improved operational efficiency, and enhanced security.

Elimination of intermediaries

The implementation of blockchain technology in business has led to the elimination of intermediaries, revolutionizing the way transactions are conducted. Traditionally, various intermediaries such as banks, brokers, and other third-party entities were involved in facilitating transactions, adding complexity, cost, and potential security risks. However, with blockchain, these intermediaries are no longer necessary as the technology enables peer-to-peer transactions, securely recorded on a decentralized ledger. This elimination of intermediaries has numerous benefits for businesses, including reduced costs, increased efficiency, improved transparency, and enhanced security. By removing the need for intermediaries, blockchain has the potential to streamline processes, eliminate unnecessary fees, and provide greater trust and accountability in business transactions.

Reduced transaction fees

Reduced transaction fees are one of the key advantages of implementing blockchain technology in business. Traditionally, businesses have to rely on intermediaries such as banks or payment processors to facilitate transactions, which often come with high fees. However, with blockchain, transactions can be conducted directly between parties without the need for intermediaries, resulting in significantly lower transaction costs. This not only saves businesses money but also enables them to offer more competitive pricing to their customers. By eliminating the middlemen and their associated fees, blockchain technology revolutionizes the way transactions are conducted, making it a game-changer for businesses across industries.

Improved Traceability

End-to-end visibility

End-to-end visibility is a crucial aspect of any successful business operation. With the implementation of blockchain technology, businesses can achieve unparalleled transparency and traceability throughout their supply chains. By recording and verifying transactions on a decentralized ledger, blockchain provides a secure and immutable record of every interaction, from the sourcing of raw materials to the delivery of the final product. This level of visibility not only enhances trust and accountability but also enables businesses to identify and address any inefficiencies or bottlenecks in their processes. With end-to-end visibility powered by blockchain, businesses can optimize their operations, streamline their supply chains, and ultimately deliver better products and services to their customers.

Auditable and verifiable records

Blockchain technology provides auditable and verifiable records, which is one of its key benefits when implemented in business. With traditional systems, it can be difficult to track and verify the authenticity of transactions and records. However, blockchain offers a transparent and immutable ledger that allows for easy auditing and verification. Every transaction and data entry is recorded on the blockchain, creating a permanent and tamper-proof record. This not only enhances trust and accountability but also simplifies compliance with regulatory requirements. By implementing blockchain, businesses can ensure the integrity and accuracy of their records, leading to increased transparency and efficiency in their operations.

Supply chain management

Supply chain management is one area where implementing blockchain technology can bring significant benefits to businesses. By utilizing blockchain, companies can achieve greater transparency and traceability throughout the supply chain process. This enables them to track the movement of goods from the point of origin to the final destination, ensuring authenticity and preventing counterfeiting. Additionally, blockchain can enhance efficiency by automating processes, reducing paperwork, and minimizing manual errors. With a decentralized and immutable ledger, businesses can establish trust among stakeholders and streamline operations, leading to improved productivity and cost savings. Overall, integrating blockchain into supply chain management has the potential to revolutionize the way businesses operate, enabling them to build more resilient and secure supply chains.

Increased Trust and Accountability

Trustless environment

A trustless environment is one of the key benefits of implementing blockchain technology in business. Unlike traditional systems that rely on intermediaries to establish trust, blockchain allows for the creation of a decentralized network where transactions are verified and recorded by multiple participants. This eliminates the need for a central authority and reduces the risk of fraud or manipulation. By providing a transparent and secure platform for conducting business transactions, blockchain technology promotes trust and confidence among all parties involved.

Smart contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automatically execute actions once the predetermined conditions are met, without the need for intermediaries. By implementing blockchain technology, businesses can leverage smart contracts to streamline and automate various processes, such as supply chain management, financial transactions, and legal agreements. This not only reduces the reliance on manual verification and paperwork but also enhances transparency, security, and efficiency. Smart contracts have the potential to revolutionize the way businesses operate by providing a decentralized, trustless, and tamper-proof solution that ensures fairness and accountability for all parties involved.

Enhanced accountability and transparency

Blockchain technology enhances accountability and transparency in business operations. By utilizing a decentralized and immutable ledger, all transactions and activities are recorded and verified, leaving no room for manipulation or fraud. This increased transparency builds trust among stakeholders, as they can easily access and validate the information stored on the blockchain. Furthermore, the use of smart contracts enables automated and secure execution of agreements, eliminating the need for intermediaries and reducing the potential for errors or disputes. Overall, implementing blockchain in business not only improves accountability but also fosters a culture of transparency that can positively impact the entire ecosystem.

Disruption in Traditional Industries

Finance and banking

Blockchain technology has revolutionized the finance and banking industry in numerous ways. One of the key benefits of implementing blockchain in this sector is increased transparency and security. With a decentralized ledger system, financial transactions can be recorded and verified in real-time, eliminating the need for intermediaries and reducing the risk of fraud. Additionally, blockchain allows for faster and more efficient cross-border transactions, as it removes the need for multiple layers of verification and reduces transaction costs. This technology also enables greater financial inclusion, as it provides access to financial services for the unbanked population. Overall, implementing blockchain in finance and banking has the potential to streamline processes, improve security, and foster financial innovation.

Supply chain and logistics

Blockchain technology has the potential to revolutionize supply chain and logistics operations. By implementing blockchain, businesses can enhance transparency, traceability, and efficiency throughout the supply chain. With a decentralized and immutable ledger, companies can securely track the movement of goods from the point of origin to the end consumer. This increased visibility not only helps in preventing fraud and counterfeit products but also enables faster identification and resolution of issues. Furthermore, blockchain can streamline logistics processes by automating documentation, reducing paperwork, and minimizing manual errors. Overall, the adoption of blockchain in supply chain and logistics can lead to improved trust, cost savings, and streamlined operations for businesses.

Healthcare and pharmaceuticals

Blockchain technology has the potential to revolutionize the healthcare and pharmaceutical industries. By implementing blockchain, healthcare providers can securely store and share patient data, ensuring privacy and data integrity. Additionally, blockchain can streamline the supply chain in the pharmaceutical industry, reducing the risk of counterfeit drugs and improving traceability. With the use of smart contracts, healthcare organizations can also automate and improve processes such as insurance claims and medical record management. Overall, the adoption of blockchain in healthcare and pharmaceuticals can lead to increased efficiency, transparency, and trust in these critical sectors.