Introduction

Definition of Blockchain Technology

Blockchain technology is a decentralized digital ledger that records transactions across multiple computers. It is designed to be transparent, secure, and tamper-proof, making it ideal for applications that require trust and transparency. The technology behind blockchain relies on cryptographic algorithms to ensure the integrity and immutability of the data stored within the blocks. By eliminating the need for intermediaries, blockchain has the potential to revolutionize various industries by providing a more efficient and cost-effective way to conduct transactions and verify information.

Brief History of Blockchain

Blockchain technology has a fascinating history that dates back to the early 2000s. It all started with the concept of a decentralized digital currency, which was first introduced by an anonymous person or group of people using the pseudonym Satoshi Nakamoto. In 2008, Nakamoto published a whitepaper titled ‘Bitcoin: A Peer-to-Peer Electronic Cash System,’ which outlined the principles and mechanisms of blockchain technology. This whitepaper laid the foundation for the development of the first blockchain-based cryptocurrency, Bitcoin, which was launched in 2009. Since then, blockchain technology has evolved and expanded beyond cryptocurrencies, finding applications in various industries such as finance, supply chain management, healthcare, and more. The history of blockchain is characterized by innovation, collaboration, and the pursuit of a decentralized and transparent future.

Importance of Blockchain Technology

Blockchain technology is becoming increasingly important in today’s digital world. It has the potential to revolutionize various industries, including finance, supply chain management, healthcare, and more. One of the key reasons why blockchain technology is important is its ability to provide transparency and security. With blockchain, transactions are recorded and verified in a decentralized manner, making it difficult for any single entity to manipulate or tamper with the data. This not only enhances trust among participants but also reduces the risk of fraud and unauthorized activities. Additionally, blockchain technology enables faster and more efficient transactions, eliminating the need for intermediaries and reducing costs. As businesses and organizations continue to explore the potential of blockchain technology, its importance in driving innovation and transforming traditional processes cannot be overstated.

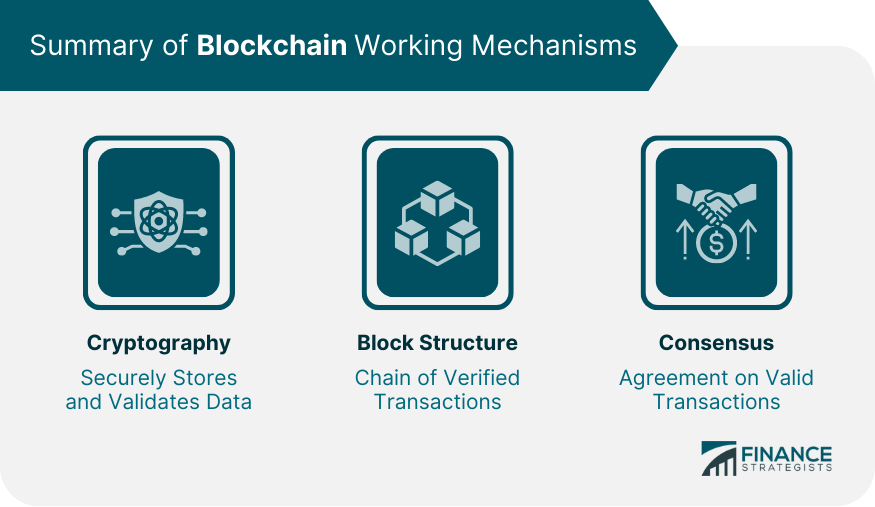

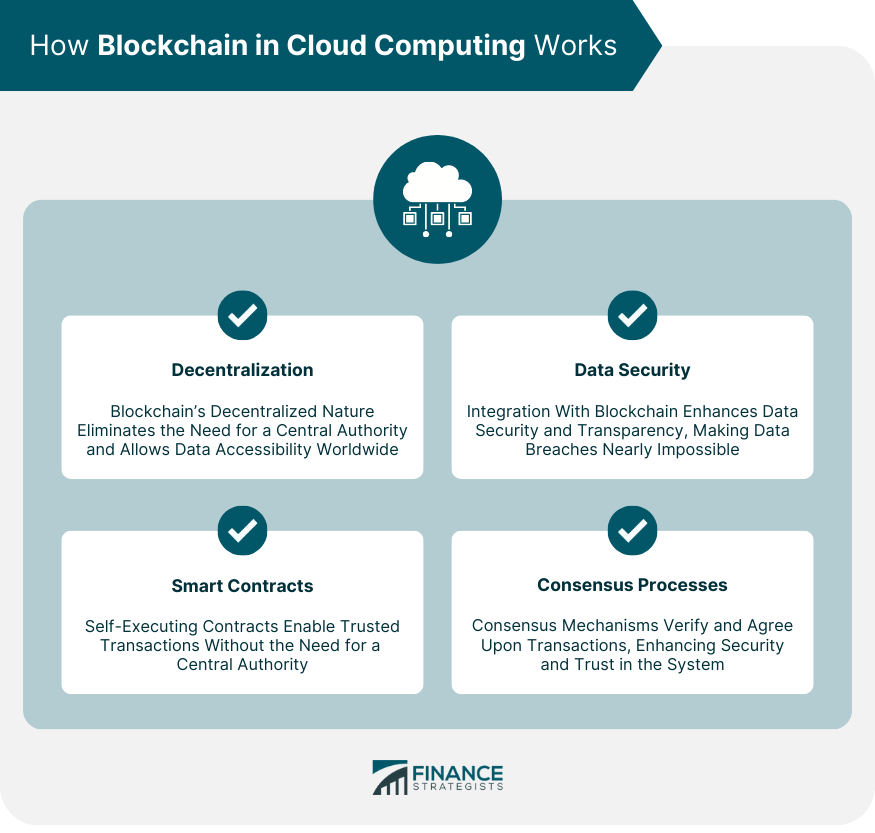

How Blockchain Works

Decentralization

Decentralization is one of the fundamental principles of blockchain technology. It refers to the distribution of authority and decision-making across a network, rather than being controlled by a central entity. In a decentralized system, every participant has access to the same information and can validate transactions independently. This eliminates the need for intermediaries and increases the security and transparency of the network. Decentralization plays a crucial role in ensuring the integrity and resilience of blockchain technology, making it resistant to censorship and single points of failure.

Consensus Mechanism

The consensus mechanism is a fundamental component of blockchain technology. It is responsible for ensuring that all participants in the network agree on the validity of transactions and the order in which they are added to the blockchain. There are various consensus mechanisms used in different blockchain platforms, such as Proof of Work (PoW), Proof of Stake (PoS), and Delegated Proof of Stake (DPoS). Each mechanism has its own advantages and disadvantages, and the choice of consensus mechanism depends on the specific needs and goals of the blockchain project. The consensus mechanism plays a crucial role in maintaining the security, decentralization, and efficiency of the blockchain network.

Cryptographic Security

Blockchain technology relies heavily on cryptographic security to ensure the integrity and confidentiality of data. Cryptography is the practice of encoding and decoding information to protect it from unauthorized access. In the context of blockchain, cryptographic techniques such as hashing and digital signatures are used to secure transactions and prevent tampering. Hashing is a process that converts data into a fixed-size string of characters, which is unique to that specific data. This allows for easy verification of data integrity, as any changes to the original data will result in a different hash value. Digital signatures, on the other hand, provide a way to verify the authenticity of a message or transaction. They use a combination of private and public keys to ensure that only the intended recipient can decrypt and verify the message. By leveraging cryptographic security, blockchain technology provides a robust and reliable platform for secure and transparent transactions.

Key Components of Blockchain

Blocks

Blocks are an essential component of blockchain technology. In simple terms, a block is a collection of data that is added to the blockchain. Each block contains a unique identifier called a hash, which is generated using a cryptographic algorithm. The hash of each block also includes the hash of the previous block, creating a chain-like structure. This ensures the integrity and security of the blockchain, as any modification to a block would require changing the hash of all subsequent blocks. Blocks serve as the building blocks of the blockchain, forming a decentralized and immutable ledger of transactions and information.

Transactions

Transactions are a fundamental aspect of blockchain technology. They involve the transfer of digital assets or information from one party to another within the blockchain network. Each transaction is securely recorded and verified by multiple participants, known as nodes, in the network. The decentralized nature of blockchain ensures that transactions are transparent, immutable, and resistant to tampering. This makes blockchain technology ideal for applications that require secure and trustless transactions, such as financial transactions, supply chain management, and smart contracts.

Nodes

Nodes are an essential component of blockchain technology. They are individual computers or devices that participate in the network by maintaining a copy of the blockchain and validating transactions. Nodes play a crucial role in ensuring the security and integrity of the blockchain by verifying and broadcasting transactions to other nodes. They also collaborate in the consensus process to reach agreement on the state of the blockchain. In addition to maintaining the blockchain, nodes can also contribute computing power for mining new blocks, depending on the consensus algorithm used. Overall, nodes are the backbone of a blockchain network, enabling decentralization, transparency, and trust in the system.

Types of Blockchain

Public Blockchain

A public blockchain is a decentralized network that allows anyone to participate and verify transactions. It is open to the public, meaning that anyone can join the network and become a node. Public blockchains are transparent, as all transactions are recorded and visible to all participants. This transparency ensures the integrity and security of the network, as any attempt to alter or manipulate the data can be easily detected. Public blockchains are often used for cryptocurrencies, such as Bitcoin and Ethereum, as they provide a secure and trustless platform for peer-to-peer transactions.

Private Blockchain

Private blockchains are a type of blockchain network that restricts access to authorized participants only. Unlike public blockchains, which are open and transparent, private blockchains are designed for specific organizations or groups. They offer increased privacy and control over the network, as only approved participants can join and validate transactions. Private blockchains are often used in industries where confidentiality and data protection are crucial, such as finance, healthcare, and supply chain management. By implementing a private blockchain, organizations can ensure that sensitive information is only accessible to authorized parties, while still benefiting from the security and efficiency of blockchain technology.

Consortium Blockchain

Consortium blockchain is a type of blockchain network where multiple organizations come together to form a governing body. Unlike public blockchains, consortium blockchains are permissioned, meaning that only approved participants can join the network and validate transactions. This type of blockchain offers increased privacy and scalability compared to public blockchains, making it ideal for industries such as finance, supply chain, and healthcare. By collaborating in a consortium blockchain, organizations can securely share data and streamline their operations, leading to improved efficiency and trust among participants.

Use Cases of Blockchain

Cryptocurrencies

Cryptocurrencies have revolutionized the financial industry by introducing a decentralized and secure method of digital transactions. These digital currencies, such as Bitcoin and Ethereum, operate on blockchain technology, which ensures transparency and immutability. Cryptocurrencies have gained significant popularity and acceptance worldwide, with an increasing number of businesses and individuals embracing them as a viable alternative to traditional forms of currency. The decentralized nature of cryptocurrencies eliminates the need for intermediaries, making transactions faster, more efficient, and cost-effective. Additionally, the underlying blockchain technology provides a high level of security, protecting users’ financial transactions from fraud and unauthorized access. As the adoption of cryptocurrencies continues to grow, they have the potential to reshape the global financial landscape and empower individuals to have more control over their financial assets.

Supply Chain Management

Blockchain technology has the potential to revolutionize supply chain management. By providing a decentralized and transparent ledger, blockchain enables real-time tracking and verification of goods throughout the entire supply chain. This not only improves efficiency and reduces costs, but also enhances trust and security in the supply chain ecosystem. With blockchain, businesses can ensure the authenticity and integrity of their products, prevent counterfeiting, and streamline processes such as inventory management, logistics, and payments. Overall, the adoption of blockchain technology in supply chain management has the potential to create a more efficient, reliable, and sustainable global supply chain.

Healthcare

Blockchain technology has the potential to revolutionize the healthcare industry. By providing a secure and transparent way to store and share medical data, blockchain can improve the efficiency and accuracy of healthcare processes. With blockchain, patients can have full control over their medical records, ensuring privacy and data security. Additionally, healthcare providers can access real-time patient information, leading to better diagnoses and personalized treatment plans. Moreover, blockchain can streamline administrative tasks, such as insurance claims and billing, reducing costs and improving overall healthcare management. As the adoption of blockchain technology in healthcare continues to grow, it holds the promise of transforming the way healthcare is delivered and experienced.

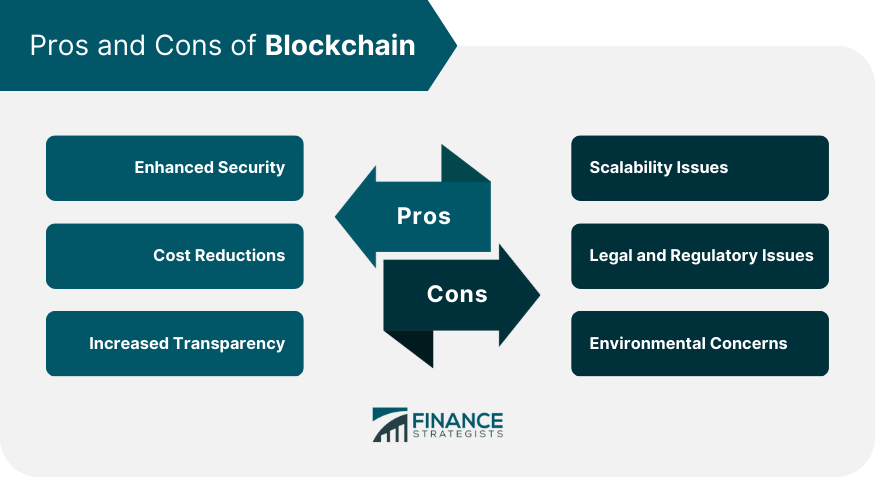

Challenges and Future of Blockchain

Scalability

Blockchain technology faces a significant challenge when it comes to scalability. As the number of transactions on a blockchain network increases, the system may experience delays and congestion. This is because each transaction needs to be verified and added to the blockchain, which requires computational power and time. Additionally, as the blockchain grows in size, it becomes more difficult for nodes to store and process the entire chain. To address this issue, various solutions have been proposed, such as sharding, off-chain transactions, and layer 2 protocols. These approaches aim to improve the scalability of blockchain technology by allowing for faster transaction processing and reducing the burden on individual nodes. However, achieving true scalability remains a complex problem that requires further research and development.

Regulatory Concerns

Regulatory concerns play a crucial role in the adoption and implementation of blockchain technology. As this innovative technology continues to disrupt traditional industries, governments and regulatory bodies around the world are grappling with how to effectively regulate and govern its use. One of the main concerns is the potential for money laundering and other illicit activities facilitated by blockchain. Additionally, privacy and data protection are also significant concerns, as the decentralized nature of blockchain can make it difficult to ensure compliance with existing regulations. However, it is important to strike a balance between regulation and innovation, as overly burdensome regulations can stifle the growth and potential benefits of blockchain technology.

Interoperability

Interoperability is a crucial aspect of blockchain technology. It refers to the ability of different blockchain networks to communicate and interact with each other seamlessly. In a decentralized ecosystem, where multiple blockchain platforms coexist, interoperability enables the transfer of assets and data between these networks. This not only enhances the efficiency and scalability of blockchain applications but also promotes collaboration and innovation across different industries. Interoperability plays a vital role in achieving the full potential of blockchain technology and realizing its promise of a decentralized and interconnected future.