Introduction

Definition of Blockchain Technology

Blockchain technology is a decentralized and distributed ledger system that allows multiple parties to record and verify transactions in a secure and transparent manner. It is often referred to as a digital ledger that is immutable, meaning once a transaction is recorded, it cannot be altered or tampered with. This technology enables trust and eliminates the need for intermediaries, such as banks or governments, as it relies on consensus algorithms and cryptography to ensure the integrity and security of the data. With its potential to revolutionize various industries, blockchain technology is gaining widespread attention and adoption.

Brief History of Blockchain

Blockchain technology has a rich and fascinating history that dates back to the early 2000s. It all started with the concept of a decentralized digital currency, which was first introduced by an anonymous person or group of people known as Satoshi Nakamoto in a whitepaper titled ‘Bitcoin: A Peer-to-Peer Electronic Cash System’ in 2008. This whitepaper laid the foundation for the development of blockchain technology as we know it today. Since then, blockchain has evolved and expanded beyond its initial use case of digital currency, with various industries recognizing its potential for secure and transparent record-keeping. Today, blockchain technology is being explored and implemented in areas such as supply chain management, healthcare, finance, and more, revolutionizing the way information is stored, verified, and shared.

Importance of Blockchain Technology

Blockchain technology is becoming increasingly important in today’s digital world. It has the potential to revolutionize various industries, including finance, supply chain management, and healthcare. One of the key reasons why blockchain technology is important is its ability to enhance security and trust in transactions. By using a decentralized network and cryptographic algorithms, blockchain ensures that data cannot be altered or tampered with, providing a high level of transparency and immutability. Additionally, blockchain technology eliminates the need for intermediaries, reducing costs and improving efficiency. As more organizations recognize the benefits of blockchain, its adoption is expected to grow rapidly, making it essential for individuals and businesses to understand its basics and potential applications.

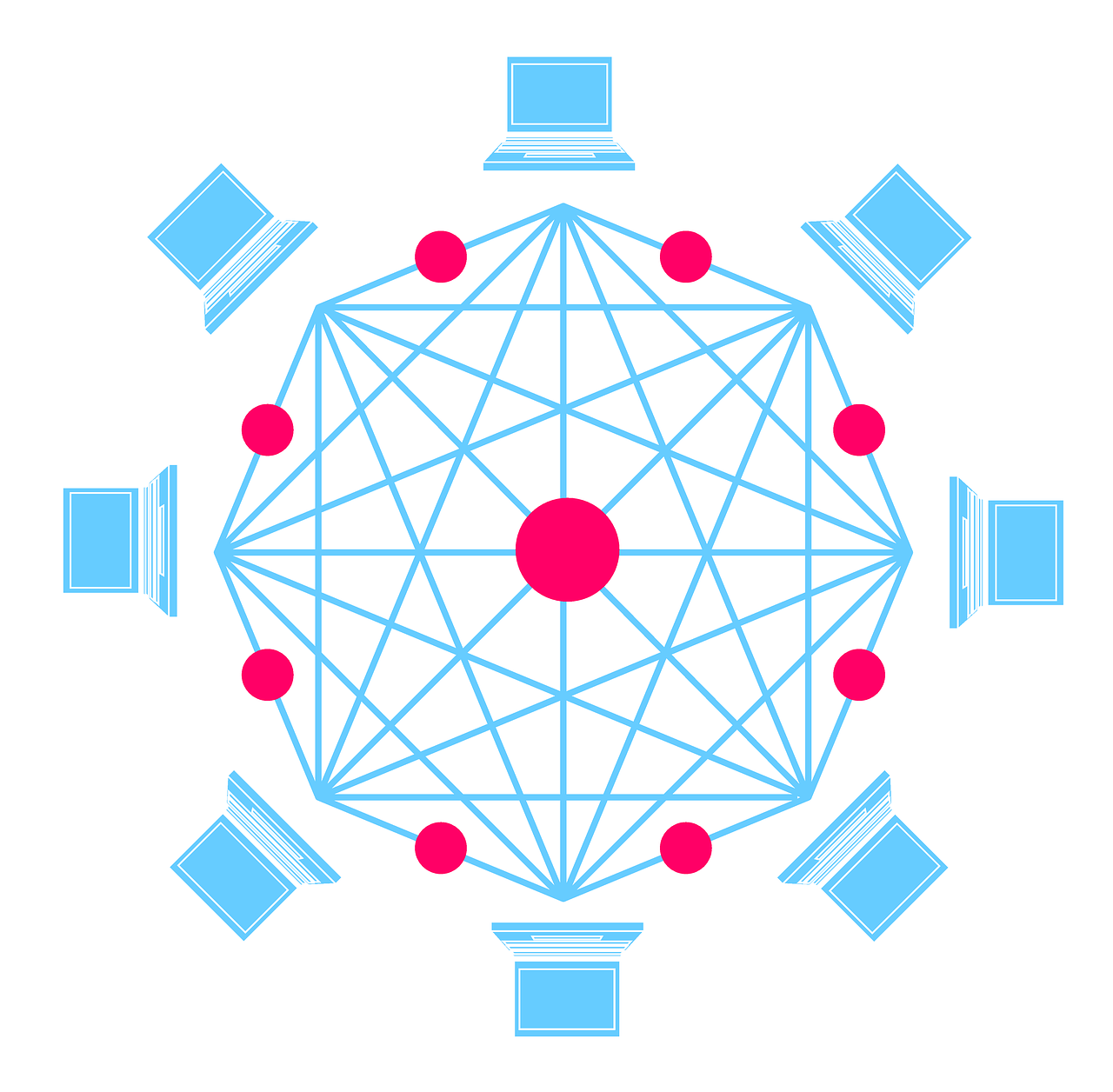

How Blockchain Works

Decentralization

Decentralization is a fundamental concept in blockchain technology. It refers to the distribution of power and control across a network of computers, rather than being concentrated in a central authority. This ensures that no single entity has complete control over the system, making it more secure and resistant to censorship. In a decentralized blockchain network, every participant has a copy of the entire blockchain, and transactions are verified and recorded by consensus among the participants. This eliminates the need for intermediaries and allows for trustless and transparent transactions. Decentralization is one of the key features that sets blockchain technology apart from traditional centralized systems.

Consensus Mechanism

Blockchain technology relies on a consensus mechanism to ensure the accuracy and security of the data stored on the blockchain. Consensus mechanisms are protocols or algorithms that enable multiple participants in a network to agree on the validity of transactions and the order in which they are added to the blockchain. One of the most commonly used consensus mechanisms is Proof of Work (PoW), where participants compete to solve complex mathematical puzzles to validate transactions. Another popular consensus mechanism is Proof of Stake (PoS), where participants are chosen to validate transactions based on the number of coins they hold. These consensus mechanisms play a crucial role in maintaining the integrity and decentralization of the blockchain network.

Cryptographic Hash Function

A cryptographic hash function is a fundamental component of blockchain technology. It is a mathematical algorithm that takes an input (or message) and produces a fixed-size string of characters, which is typically a sequence of numbers and letters. The output, known as the hash value or hash code, is unique to the input data and is used to verify the integrity and authenticity of the information stored in a blockchain. By using a cryptographic hash function, blockchain networks can ensure that data cannot be tampered with or altered without detection. This makes it an essential element in establishing trust and security within the blockchain ecosystem.

Key Components of Blockchain

Blocks

Blocks are an essential component of blockchain technology. They serve as containers that store and record multiple transactions. Each block contains a unique identifier, a timestamp, and a reference to the previous block, creating a chain-like structure. The information within a block is encrypted and cannot be altered, ensuring the integrity and security of the data. Blocks are added to the blockchain through a consensus mechanism, such as proof-of-work or proof-of-stake, which validates and verifies the transactions before they are added to the chain. This decentralized and transparent nature of blocks makes blockchain technology highly secure and resistant to tampering or fraud.

Transactions

Transactions are a fundamental aspect of blockchain technology. They represent the transfer of digital assets or information from one party to another within a blockchain network. Each transaction is recorded and verified by multiple participants, known as nodes, ensuring its validity and preventing any fraudulent activity. Transactions in blockchain technology are secure, transparent, and immutable, providing a reliable and efficient method for conducting business and exchanging value. With the decentralized nature of blockchain, transactions can be conducted without the need for intermediaries, reducing costs and increasing the speed of transactions. Overall, transactions play a crucial role in the functionality and success of blockchain technology, enabling secure and efficient digital transactions across various industries and use cases.

Nodes

Nodes are an essential component of the blockchain network. They are individual computers or devices that participate in the validation and verification of transactions. Each node stores a copy of the entire blockchain, ensuring the decentralized nature of the technology. Nodes communicate with each other to maintain consensus and ensure the integrity of the network. They play a crucial role in the security and efficiency of blockchain technology, as they contribute to the validation and propagation of new transactions and blocks throughout the network.

Types of Blockchain

Public Blockchain

Public blockchains are decentralized networks where anyone can participate and validate transactions. This type of blockchain is open to the public, allowing for transparency and trust among participants. Public blockchains are often used for cryptocurrencies like Bitcoin and Ethereum, where anyone can create an account and participate in the network. The security of public blockchains is maintained through consensus mechanisms, such as proof of work or proof of stake, which ensure that transactions are valid and secure. Overall, public blockchains play a crucial role in enabling decentralized and transparent systems.

Private Blockchain

A private blockchain, as the name suggests, is a blockchain that is restricted to a specific group or organization. Unlike public blockchains, which are open to anyone, private blockchains require permission to join and participate. This level of control allows for increased privacy and security, as only trusted participants have access to the network. Private blockchains are often used by businesses and enterprises to streamline their operations, facilitate secure transactions, and maintain confidentiality of sensitive information. By implementing a private blockchain, organizations can ensure that their data remains secure while still benefiting from the transparency and immutability of blockchain technology.

Consortium Blockchain

Consortium blockchain is a type of blockchain network where multiple organizations come together to form a governing body. Unlike public blockchains, consortium blockchains are permissioned, meaning that only approved participants can join the network and validate transactions. This type of blockchain offers a higher level of privacy and scalability compared to public blockchains, making it ideal for industries that require a certain level of trust among its participants. In a consortium blockchain, the governing body sets the rules and regulations, ensuring that all participants adhere to the agreed-upon standards. This collaborative approach allows for efficient decision-making and consensus among the consortium members.

Applications of Blockchain

Cryptocurrencies

Cryptocurrencies have revolutionized the financial industry by introducing a decentralized and secure method of conducting transactions. These digital currencies, such as Bitcoin and Ethereum, utilize blockchain technology to ensure transparency, immutability, and privacy. With the rise of cryptocurrencies, individuals and businesses can now easily transfer funds globally without the need for intermediaries like banks. Moreover, cryptocurrencies have opened up new opportunities for investment and have sparked innovation in various sectors. As the popularity of cryptocurrencies continues to grow, it is important to understand their underlying technology and the potential impact they can have on the future of finance.

Supply Chain Management

Supply chain management is a crucial aspect of any business, and the implementation of blockchain technology can greatly enhance its efficiency and transparency. With blockchain, companies can track and trace products throughout the entire supply chain, from raw materials to the end consumer. This allows for greater visibility and accountability, as each transaction and movement of goods is recorded on the blockchain. Additionally, blockchain technology can help prevent fraud and counterfeiting by ensuring that every step in the supply chain is verified and authenticated. By leveraging the power of blockchain, businesses can streamline their supply chain processes, reduce costs, and build trust with their customers.

Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into lines of code. These contracts automatically execute when the conditions specified in the code are met. By eliminating the need for intermediaries, smart contracts provide a secure and transparent way to facilitate transactions and agreements. They are a key component of blockchain technology, enabling decentralized applications and enabling trustless interactions between parties. With the ability to automate processes and remove the need for manual intervention, smart contracts have the potential to revolutionize various industries, including finance, supply chain management, and real estate.

Challenges and Future of Blockchain

Scalability

Scalability is a critical aspect of blockchain technology. As the popularity and adoption of blockchain continue to grow, it is essential to address the issue of scalability. Scalability refers to the ability of a blockchain network to handle a large number of transactions efficiently. With the increasing number of users and transactions on the blockchain, it is crucial to have a scalable solution that can handle the load without compromising on performance. Various approaches, such as sharding, sidechains, and off-chain transactions, are being explored to improve the scalability of blockchain technology. These solutions aim to enhance the throughput and speed of transactions, making blockchain technology more practical for widespread use in various industries.

Security

Blockchain technology offers a high level of security, making it one of the most secure ways to store and transfer data. The decentralized nature of blockchain ensures that no single entity has control over the entire network, reducing the risk of hacking or data manipulation. Additionally, the use of cryptographic algorithms and consensus mechanisms further enhances the security of blockchain. With its transparent and immutable nature, blockchain technology provides a tamper-proof system that can be trusted for various applications, including financial transactions, supply chain management, and identity verification.

Regulatory Concerns

Regulatory concerns surrounding blockchain technology have become a prominent topic of discussion in recent years. As the technology continues to evolve and gain widespread adoption, governments and regulatory bodies are grappling with how to effectively oversee and regulate this decentralized and transparent system. One of the main concerns is the potential for illicit activities, such as money laundering and terrorism financing, facilitated by the anonymity and pseudonymity provided by blockchain. Additionally, the cross-border nature of blockchain transactions presents challenges for regulators in terms of jurisdiction and enforcement. However, it is important to strike a balance between regulatory oversight and fostering innovation to fully harness the potential of blockchain technology.