Introduction

What is Blockchain Technology?

Blockchain technology is a revolutionary concept that has gained significant attention in recent years. It is essentially a decentralized and transparent digital ledger that records transactions across multiple computers. The key feature of blockchain technology is its ability to ensure security and trust without the need for intermediaries. By using cryptographic techniques, each transaction is verified and added to a chain of previous transactions, creating an immutable and tamper-proof record. This technology has the potential to transform various industries, including finance, supply chain management, and healthcare, by providing a more efficient, secure, and transparent way of conducting transactions.

History of Blockchain

The history of blockchain dates back to 2008 when an anonymous person or group of people known as Satoshi Nakamoto introduced the concept in a whitepaper titled ‘Bitcoin: A Peer-to-Peer Electronic Cash System’. This whitepaper outlined the foundational principles of blockchain technology and how it could be used to create a decentralized digital currency. Since then, blockchain has evolved and expanded beyond its original application in cryptocurrencies, finding use cases in various industries such as finance, supply chain management, and healthcare. Today, blockchain technology is recognized for its potential to revolutionize the way we conduct transactions, store data, and establish trust in a digital world.

Why is Blockchain Important?

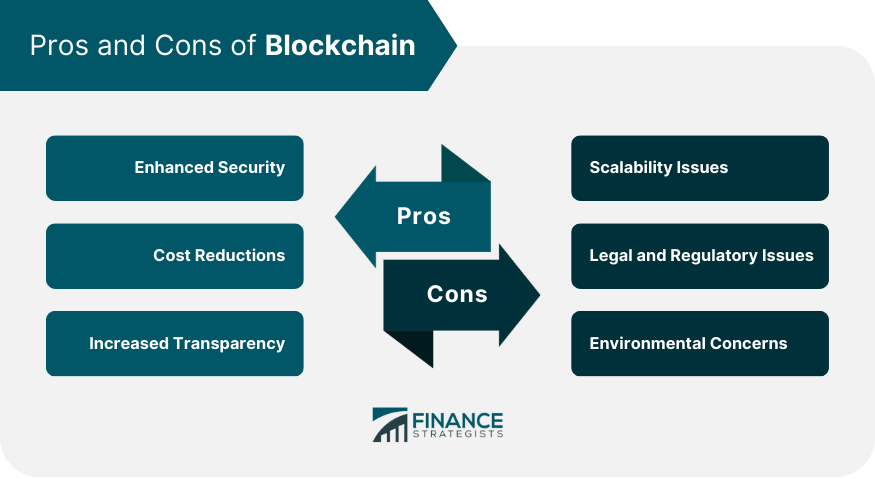

Blockchain technology is important because it provides a decentralized and secure way to record and verify transactions. With traditional systems, there is often a need for intermediaries such as banks or government institutions to validate transactions. However, with blockchain, transactions can be directly recorded on a distributed ledger that is accessible to all participants in the network. This eliminates the need for intermediaries and reduces the risk of fraud or manipulation. Additionally, blockchain technology offers transparency, as all transactions are visible to all participants, ensuring accountability and trust. Furthermore, blockchain has the potential to revolutionize various industries, including finance, supply chain management, and healthcare, by streamlining processes, reducing costs, and enabling new business models. As such, understanding the basics of blockchain technology is crucial for anyone interested in the future of digital innovation.

How Does Blockchain Work?

Decentralization

Decentralization is one of the fundamental principles of blockchain technology. Unlike traditional centralized systems, where a single authority has control over the data and transactions, blockchain operates on a distributed network of computers called nodes. These nodes work together to validate and record transactions, ensuring that no single entity can manipulate or control the system. This decentralized nature of blockchain technology not only enhances security but also promotes transparency and trust among participants. By removing the need for intermediaries, blockchain enables peer-to-peer transactions, making it a revolutionary technology with the potential to disrupt various industries.

Consensus Mechanisms

Consensus mechanisms play a crucial role in blockchain technology. They are the algorithms or protocols that enable multiple participants in a decentralized network to agree on the state of the blockchain. In other words, consensus mechanisms ensure that all participants reach a consensus on the validity of transactions and the order in which they are added to the blockchain. There are various consensus mechanisms used in different blockchain networks, such as Proof of Work (PoW), Proof of Stake (PoS), and Delegated Proof of Stake (DPoS). Each consensus mechanism has its own advantages and disadvantages, and the choice of consensus mechanism depends on the specific requirements of the blockchain network. Overall, consensus mechanisms are essential for maintaining the integrity and security of blockchain technology.

Cryptographic Security

Cryptographic security is a fundamental aspect of blockchain technology. It provides the necessary tools and techniques to ensure the confidentiality, integrity, and authenticity of data stored on the blockchain. Through the use of advanced cryptographic algorithms, such as hash functions and digital signatures, blockchain networks are able to secure transactions and prevent unauthorized access or tampering. This robust security framework makes blockchain technology highly resistant to hacking and fraud, making it a trusted solution for various industries, including finance, supply chain, and healthcare.

Types of Blockchains

Public Blockchains

Public blockchains are a fundamental aspect of blockchain technology. These are decentralized networks where anyone can participate and verify transactions. The transparency and immutability of public blockchains make them ideal for applications requiring trust and security. In a public blockchain, all transactions are visible to the public, ensuring accountability and preventing fraud. Additionally, public blockchains enable the development of decentralized applications (DApps) and smart contracts, revolutionizing industries such as finance, supply chain management, and healthcare. As more individuals and organizations recognize the potential of public blockchains, their adoption continues to grow, paving the way for a more transparent and efficient future.

Private Blockchains

Private blockchains are a variant of blockchain technology that restricts access to the network and its data to a specific group of participants. Unlike public blockchains, which are open and accessible to anyone, private blockchains are designed for use within organizations or among a select group of trusted entities. The main advantage of private blockchains is the enhanced privacy and control they offer, as participants have more control over who can join the network and access the data. This makes private blockchains particularly appealing to industries that require strict confidentiality and data protection, such as finance, healthcare, and supply chain management.

Consortium Blockchains

Consortium blockchains, also known as private blockchains, are a type of blockchain network where the consensus process is controlled by a group of organizations rather than a single entity. In a consortium blockchain, the participating organizations collaborate to validate transactions and maintain the integrity of the network. This type of blockchain is often used in industries where privacy and permissioned access are important, such as finance, healthcare, and supply chain management. By allowing a select group of participants to control the consensus process, consortium blockchains offer increased scalability, privacy, and efficiency compared to public blockchains.

Applications of Blockchain

Cryptocurrencies

Cryptocurrencies are digital or virtual currencies that use cryptography for security. They are decentralized and operate on a technology called blockchain. Cryptocurrencies enable secure and anonymous transactions, making them a popular choice for online payments and investments. Some well-known cryptocurrencies include Bitcoin, Ethereum, and Litecoin. These digital currencies have gained significant attention in recent years and have the potential to revolutionize the financial industry.

Supply Chain Management

Supply chain management is one of the key areas where blockchain technology has the potential to revolutionize traditional processes. With its decentralized and transparent nature, blockchain can provide an immutable and auditable record of every transaction and movement within a supply chain. This not only enhances visibility and traceability but also ensures trust and authenticity throughout the entire process. By eliminating intermediaries and reducing paperwork, blockchain can streamline supply chain operations, reduce costs, and eliminate the risk of fraud and counterfeiting. Additionally, smart contracts can automate and enforce compliance with predefined rules, further enhancing efficiency and accountability. As businesses increasingly recognize the benefits of blockchain in supply chain management, we can expect to see widespread adoption and transformation in this industry.

Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into lines of code. These contracts automatically execute when the predefined conditions are met, ensuring transparency, efficiency, and trustworthiness. By eliminating the need for intermediaries, smart contracts enable parties to interact directly, reducing costs and streamlining processes. They have gained significant attention in the blockchain space due to their potential to revolutionize various industries, such as finance, supply chain management, and real estate. With their ability to automate and enforce agreements, smart contracts are paving the way for a decentralized and secure future.

Challenges and Limitations

Scalability

Scalability is a crucial aspect of blockchain technology that has been a topic of discussion in recent years. As the popularity and adoption of blockchain continue to grow, the need for scalable solutions becomes more evident. Scalability refers to the ability of a blockchain network to handle an increasing number of transactions without compromising its performance or efficiency. The challenge lies in finding a balance between decentralization and scalability, as increasing the network’s capacity often comes at the cost of centralization. Various approaches, such as sharding, sidechains, and off-chain solutions, are being explored to address this scalability issue and enable blockchain technology to support a larger user base and a wider range of applications.

Energy Consumption

Blockchain technology has gained significant attention in recent years due to its potential to revolutionize various industries. However, one concern that has been raised is its energy consumption. The process of mining, which is essential for maintaining the blockchain network, requires a substantial amount of computational power and, consequently, energy. This has led to debates about the environmental impact of blockchain technology. While some argue that the energy consumption is justified by the benefits it brings, others advocate for more energy-efficient alternatives. As the technology continues to evolve, finding a balance between innovation and sustainability will be crucial for the widespread adoption of blockchain technology.

Regulatory Concerns

Regulatory concerns surrounding blockchain technology have become a prominent topic of discussion in recent years. As the technology continues to evolve and gain mainstream adoption, governments and regulatory bodies are grappling with how to effectively regulate this innovative and decentralized system. One of the main concerns is the potential for money laundering and illicit activities facilitated by blockchain. While blockchain offers transparency and immutability, it also presents challenges in terms of identifying and tracking individuals involved in illegal transactions. Additionally, the cross-border nature of blockchain transactions raises questions about jurisdiction and regulatory harmonization. Despite these challenges, many governments are recognizing the potential benefits of blockchain technology and are working towards creating a balanced regulatory framework that fosters innovation while protecting against misuse. As the technology matures, it is expected that regulatory concerns will continue to be addressed and refined, paving the way for a more secure and trustworthy blockchain ecosystem.

Future of Blockchain

Integration with Internet of Things (IoT)

Blockchain technology has the potential to revolutionize the way the Internet of Things (IoT) operates. By integrating blockchain with IoT devices, a new level of trust, security, and transparency can be achieved. With blockchain, IoT devices can securely communicate and transact with each other, eliminating the need for intermediaries and reducing the risk of data breaches. Additionally, blockchain’s decentralized nature ensures that no single entity has control over the data, making it more resilient to cyber attacks. This integration also enables the creation of smart contracts, which can automate and enforce agreements between IoT devices, further enhancing efficiency and reliability. Overall, the integration of blockchain technology with the Internet of Things holds immense potential to transform various industries and improve the way devices interact and exchange data.

Blockchain in Finance

Blockchain technology has revolutionized the financial industry, providing a secure and transparent platform for transactions. In finance, blockchain has the potential to streamline processes, reduce costs, and enhance security. With blockchain, financial institutions can eliminate intermediaries, such as banks, and conduct direct peer-to-peer transactions. This not only speeds up the transaction process but also reduces the risk of fraud and human error. Additionally, blockchain enables real-time auditing and verification of financial transactions, ensuring accuracy and accountability. As a result, blockchain technology has the power to transform traditional financial systems and pave the way for a more efficient and inclusive financial ecosystem.

Potential Disruptions

Blockchain technology has the potential to disrupt various industries and sectors. Its decentralized and transparent nature eliminates the need for intermediaries, making transactions more efficient and secure. In the financial sector, blockchain can revolutionize the way we make payments, transfer assets, and manage identities. Additionally, blockchain has the potential to transform supply chain management by providing a transparent and immutable record of every transaction, ensuring authenticity and preventing fraud. Moreover, blockchain technology can disrupt the healthcare industry by securely storing and sharing patient data, improving interoperability and privacy. With its wide-ranging applications, blockchain technology is poised to bring about significant disruptions across various sectors.