Introduction

Definition of Blockchain

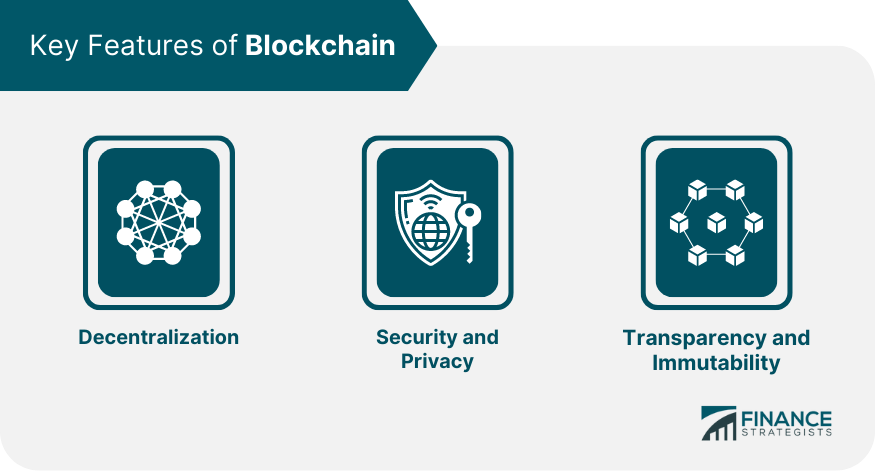

Blockchain is a decentralized and distributed ledger technology that allows multiple parties to maintain a shared database without the need for a central authority. It is designed to be transparent, secure, and immutable, making it ideal for recording and verifying transactions. The technology behind blockchain relies on cryptographic algorithms to ensure the integrity and confidentiality of the data. By eliminating the need for intermediaries, blockchain has the potential to revolutionize various industries, including finance, supply chain management, and healthcare, by increasing efficiency, reducing costs, and enhancing trust between participants.

Overview of Regulatory Challenges

Blockchain technology has gained significant attention in recent years, revolutionizing various industries. However, its rapid growth has also posed numerous regulatory challenges that need to be addressed. The overview of regulatory challenges in the context of blockchain encompasses a wide range of issues, including data privacy, security, identity verification, and financial regulations. These challenges arise due to the decentralized nature of blockchain, which makes it difficult to regulate and monitor transactions. As governments and regulatory bodies strive to keep up with the advancements in blockchain technology, it is crucial to establish clear guidelines and frameworks to ensure the responsible and secure implementation of this innovative technology.

Importance of Navigating Regulatory Challenges

The importance of navigating regulatory challenges in the blockchain industry cannot be overstated. As blockchain technology continues to disrupt various sectors, it also presents unique regulatory challenges. These challenges arise due to the decentralized and transparent nature of blockchain, which often conflicts with traditional regulatory frameworks. Navigating these challenges is crucial for businesses and individuals operating in the blockchain space to ensure compliance, mitigate risks, and foster innovation. By understanding and adhering to regulatory requirements, stakeholders can build trust, attract investment, and contribute to the responsible and sustainable growth of the blockchain ecosystem.

Regulatory Landscape

Current Regulatory Frameworks

Blockchain technology has gained significant attention in recent years, with its potential to revolutionize various industries. However, the regulatory landscape surrounding blockchain remains uncertain and complex. The current regulatory frameworks are struggling to keep pace with the rapid advancements in technology, posing challenges for businesses and individuals navigating the blockchain space. The decentralized nature of blockchain and its cross-border capabilities make it difficult for regulators to establish uniform rules and guidelines. As a result, businesses operating in the blockchain industry face a patchwork of regulations that vary from country to country. This lack of regulatory clarity hinders innovation and investment in the blockchain sector. To address these challenges, stakeholders, including governments, regulatory bodies, and industry players, need to collaborate and develop comprehensive and adaptable regulatory frameworks that strike a balance between consumer protection and fostering innovation.

Key Regulatory Bodies

Blockchain technology has gained significant attention in recent years, but its adoption is not without challenges. One of the key hurdles that blockchain projects face is navigating the regulatory landscape. As blockchain operates in a decentralized and borderless manner, it often falls outside the jurisdiction of traditional regulatory bodies. However, there are several key regulatory bodies that play a crucial role in overseeing and shaping the use of blockchain technology. These bodies include financial regulatory agencies, such as the Securities and Exchange Commission (SEC) in the United States and the Financial Conduct Authority (FCA) in the United Kingdom, as well as international organizations like the Financial Action Task Force (FATF). These regulatory bodies aim to strike a balance between fostering innovation and ensuring consumer protection, while also addressing concerns related to money laundering, fraud, and market manipulation. Navigating the regulatory challenges of blockchain requires a deep understanding of the evolving regulatory landscape and proactive engagement with these key bodies to ensure compliance and promote responsible blockchain adoption.

Challenges in Regulatory Compliance

Blockchain technology presents unique challenges in regulatory compliance. As a decentralized and transparent system, blockchain raises questions about data privacy, security, and identity verification. Additionally, the global nature of blockchain networks requires navigating various regulatory frameworks and jurisdictions. Ensuring compliance with anti-money laundering (AML) and know your customer (KYC) regulations is particularly complex in the context of blockchain. As the technology continues to evolve, regulators and industry participants must work together to address these challenges and establish a robust regulatory framework that fosters innovation while protecting consumers and maintaining trust in the system.

Privacy and Data Protection

Data Privacy Regulations

Data privacy regulations play a crucial role in the adoption and implementation of blockchain technology. As blockchain allows for the transparent and immutable storage of data, it raises concerns about the protection and privacy of personal information. To address these concerns, governments around the world have been actively working on developing and implementing data privacy regulations that are applicable to blockchain. These regulations aim to strike a balance between the benefits of blockchain technology and the need to safeguard individuals’ privacy rights. By providing clear guidelines and requirements, data privacy regulations help businesses and organizations navigate the complex landscape of blockchain and ensure compliance with privacy laws.

Challenges in Data Protection

Blockchain technology presents unique challenges in data protection. One of the main challenges is ensuring the privacy and security of sensitive information stored on the blockchain. As blockchain is a decentralized and immutable ledger, it is difficult to modify or delete data once it is recorded. This raises concerns about the storage and protection of personal data, as well as compliance with data protection regulations. Another challenge is the need to strike a balance between transparency and privacy. While blockchain offers transparency by allowing all participants to view and verify transactions, it also raises concerns about the exposure of sensitive information. Organizations must navigate these challenges to ensure that data protection measures are in place while harnessing the benefits of blockchain technology.

Impact of Blockchain on Privacy

Blockchain technology has revolutionized various industries, including finance, supply chain, and healthcare. However, its impact on privacy is a subject of concern. While blockchain offers transparency and immutability, it also poses challenges to maintaining privacy. The decentralized nature of blockchain makes it difficult to control access to information, raising questions about data protection and confidentiality. Moreover, the use of public keys in blockchain transactions can potentially expose personal information. As organizations and governments navigate the regulatory challenges of blockchain, finding a balance between transparency and privacy becomes crucial. Implementing robust privacy measures and establishing regulatory frameworks that address these concerns will be essential for the widespread adoption of blockchain technology.

Security and Fraud Prevention

Cybersecurity Risks

Blockchain technology has revolutionized various industries, but it also comes with its fair share of cybersecurity risks. As the decentralized nature of blockchain eliminates the need for intermediaries, it opens up new vulnerabilities that hackers can exploit. One of the main risks is the potential for unauthorized access to private keys, which can lead to the theft of digital assets. Additionally, smart contracts, which are self-executing agreements on the blockchain, can be susceptible to coding errors and vulnerabilities. These risks highlight the importance of implementing robust security measures and conducting regular audits to ensure the integrity and safety of blockchain systems.

Fraudulent Activities in Blockchain

Fraudulent activities in the blockchain industry have become a significant concern in recent years. As blockchain technology continues to gain traction and revolutionize various sectors, it has also attracted the attention of fraudsters who seek to exploit its decentralized nature and anonymity. From initial coin offering (ICO) scams to Ponzi schemes and money laundering, the blockchain has witnessed a range of fraudulent activities. These activities not only undermine the trust and integrity of the blockchain ecosystem but also pose serious risks to investors and users. As regulators grapple with the challenges of overseeing this nascent technology, it is crucial to develop robust frameworks and regulations to detect, prevent, and deter fraudulent activities in blockchain effectively.

Regulatory Measures for Security

Blockchain technology has introduced numerous benefits, but it also poses unique regulatory challenges. To ensure the security of blockchain networks, regulatory measures are essential. These measures aim to protect against fraudulent activities, data breaches, and other security risks. One such measure is the implementation of Know Your Customer (KYC) protocols, which require participants to verify their identities. Additionally, regulatory bodies are working towards establishing clear guidelines for Initial Coin Offerings (ICOs) to prevent scams and protect investors. By implementing these regulatory measures, the blockchain industry can achieve a balance between innovation and security.

Smart Contracts and Legal Implications

Understanding Smart Contracts

Smart contracts are self-executing agreements with the terms of the agreement directly written into lines of code. These contracts automatically execute when the conditions specified in the code are met. Understanding smart contracts is crucial in navigating the regulatory challenges of blockchain. As smart contracts are becoming more prevalent in various industries, it is important to grasp their functionality and implications. By understanding how smart contracts work, businesses and individuals can effectively utilize blockchain technology while complying with regulatory requirements.

Enforceability of Smart Contracts

The enforceability of smart contracts is a crucial aspect to consider when navigating the regulatory challenges of blockchain technology. Smart contracts are self-executing agreements with the terms of the agreement directly written into lines of code. While they offer numerous benefits, such as increased efficiency and transparency, their enforceability has raised legal concerns. Traditional contract law may not fully address the unique characteristics of smart contracts, leading to uncertainties regarding their validity and enforceability. As blockchain technology continues to evolve, regulators and legal experts are working to develop frameworks and guidelines to ensure the enforceability of smart contracts and provide clarity to businesses and individuals engaging in blockchain transactions.

Legal Challenges and Considerations

Blockchain technology presents unique legal challenges and considerations that organizations must navigate. One of the key challenges is the lack of established regulations and legal frameworks surrounding blockchain. This creates uncertainty and ambiguity in areas such as data privacy, intellectual property rights, and jurisdictional issues. Additionally, the decentralized nature of blockchain raises questions about liability and accountability. Organizations must also consider compliance with existing regulations, such as anti-money laundering and know-your-customer requirements. Despite these challenges, many organizations are exploring the potential of blockchain technology and working towards developing legal solutions to address these concerns.

International Regulatory Harmonization

Divergent Regulatory Approaches

Blockchain technology has gained significant attention in recent years, with its potential to revolutionize various industries. However, one of the biggest challenges faced by the blockchain industry is the lack of uniform regulatory frameworks across different jurisdictions. This has resulted in divergent regulatory approaches towards blockchain and cryptocurrencies. Some countries have embraced blockchain technology and implemented favorable regulations to encourage its growth and innovation. On the other hand, some jurisdictions have taken a more cautious approach, imposing strict regulations or even banning certain aspects of blockchain and cryptocurrencies. This divergence in regulatory approaches creates challenges for businesses and individuals operating in the blockchain space, as they need to navigate through a complex web of regulations to ensure compliance and avoid legal risks. As the blockchain industry continues to evolve, it is crucial for regulators to collaborate and establish harmonized regulatory frameworks that promote innovation while addressing concerns related to security, privacy, and financial stability.

Need for International Cooperation

The rapid growth and adoption of blockchain technology has highlighted the need for international cooperation in addressing the regulatory challenges it presents. As blockchain operates on a decentralized and borderless network, it becomes imperative for countries to collaborate and harmonize their regulatory frameworks to ensure the smooth functioning of this technology. Without international cooperation, there is a risk of fragmented regulations that could hinder innovation and limit the potential benefits of blockchain across borders. By working together, countries can establish common standards, share best practices, and develop regulatory frameworks that promote innovation while addressing concerns such as data privacy, security, and consumer protection. International cooperation is essential to create an enabling environment for blockchain technology to thrive and unlock its full potential in driving economic growth and transformation on a global scale.

Challenges in Achieving Harmonization

Blockchain technology has the potential to revolutionize various industries, but it also presents significant regulatory challenges. Achieving harmonization in the regulatory landscape is one of the key hurdles that need to be overcome. With different countries and jurisdictions having their own set of regulations and policies, it becomes difficult to create a unified framework for blockchain adoption. The lack of standardized regulations can lead to confusion and uncertainty for businesses and individuals looking to leverage blockchain technology. Additionally, the rapid pace of technological advancements in the blockchain space further complicates the regulatory landscape. Governments and regulatory bodies must work together to address these challenges and develop a cohesive regulatory framework that fosters innovation while ensuring consumer protection and data privacy.